An investment opportunity can be shaped in several ways and many principles and processes are similar across the opportunities. Typically, when an investment opportunity is identified and subsequently explored, a structured transaction process is initiated. A multidisciplinary team of various advisors is assembled, each with their individual expertise and focus areas such as financial, legal, tax, commercial, and technical. By nature, these categories are very different, thus, the specific content and due diligence process vary greatly.

As such, it must be noted that this article solely focuses on the two latter areas, i.e., commercial, and technical due diligence. As both topics are too comprehensive to cover in detail, the article will more specially cover the following crucial sub-topics: Business Case Assumptions, Contractual Due Diligence and Technical Asset Review. In the context of this article, the case is illustrated with buy-side due diligence in relation to an operational, stand-alone wind farm. The due diligence process is similar for other renewable assets.

Why should you read this article?

- To gain further insight into how a due diligence process for a renewable project is conducted, gain awareness of common key assessment areas, and understand the importance of due diligence within a transaction

- Understand how conducting a thorough due diligence in the transaction process can lead to greater awareness of key project risks enabling risk mitigation measures

- To recognize the complexity of conducting due diligence, exemplified through a few selected key areas and understand how these can impact the valuation assumptions

Why conduct due diligence?

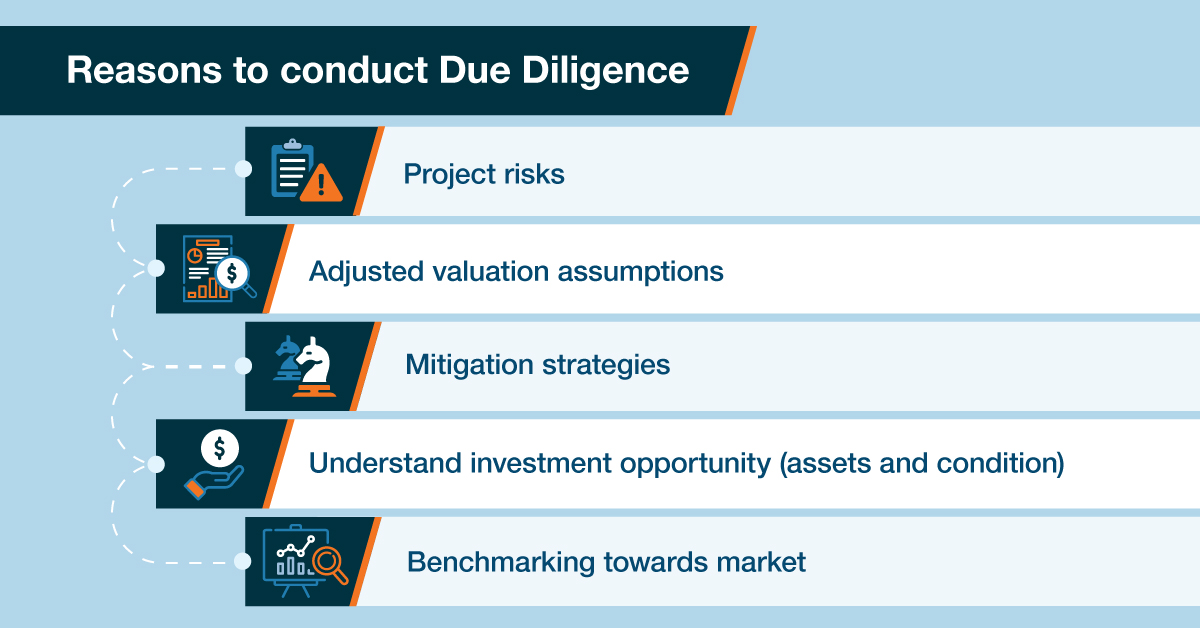

Prior to making a final investment decision it is crucial that the decision makers are well informed and equipped to make the decision on an educated basis to limit or even avoid unforeseen events with a negative impact at a later stage. This is where the due diligence process comes into play.

Without conducting due diligence, the given investor would solely have to rely on the information provided by the vendor, which might be positively skewed or might leave out relevant information to maximize the vendor’s return.

Thus, the purpose of conducting due diligence is to inform the decision makers and ensure the given investment opportunity is thoroughly scrutinized to identify and highlight major risks and discrepancies and explain how they might be mitigated. Furthermore, the findings will often be reflected in the valuation assumptions which are to be adjusted as a result, leading to a more accurate and appropriate valuation.

What is technical and commercial due diligence?

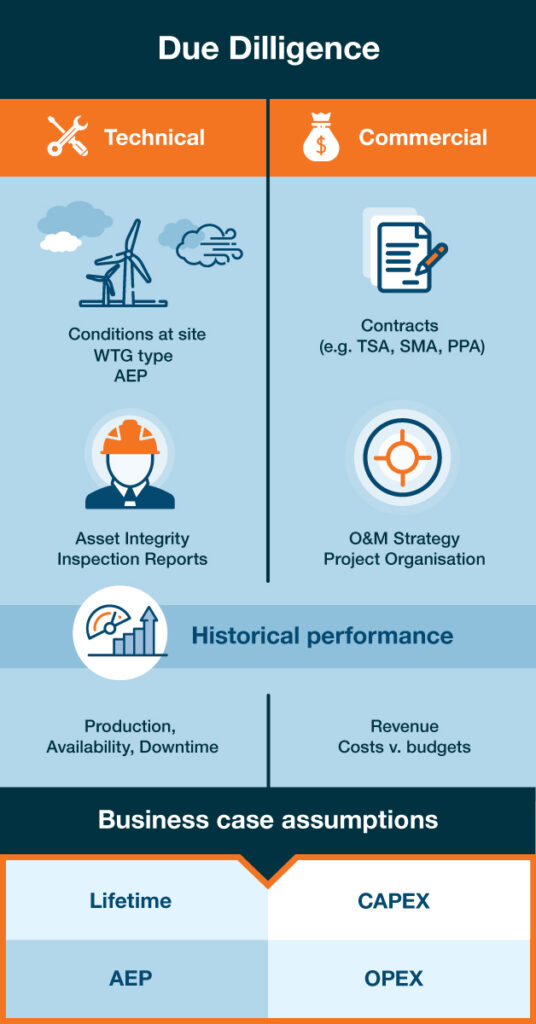

As illustrated in the figure below, the technical due diligence focuses on the key areas related to the condition and performance of the assets. Areas to be further elaborated within this article include asset integrity, remaining asset lifetime, annual energy production (AEP), and availability levels.

Commercial due diligence, on the other hand, focuses on economic and strategic key areas related to the assets such as profit and loss (P&L) statement of the assets including operational expenditures (OPEX) and revenue, contractual setup including, pricing, cost coverage, and terms and conditions.

The two areas are closely interlinked, and the importance of conducting both is underlined by the fact that the combination of the two assessments form the foundation of several key business case assumptions.

For both areas, the first step in the process is to identify which documentation to request from the vendor.

A closer look at the due diligence process

Before being able to conduct technical due diligence, certain key documents must be requested from and made available by the vendor. These include, but are not limited to:

- Site suitability assessment & main component load calculations from the OEM

- Design certifications

- Grid connection agreement

- Major component failure rate assumptions

- Energy yield studies

- Inspection reports

- Historical operational reports including production, losses, and availability

- Service logs

- Maintenance plan and scheduled overhauls

- Occurrence of major component breakdowns and exchanges

- TSA Schedules

These documents are particularly relevant for various reasons, however, common to all is that by reviewing these, the historical performance and physical condition and of the assets become apparent. As a potential new owner of the assets, it is of utmost importance to learn how the assets have performed historically, how they have been maintained, whether any structural flaws can be determined etc. More specifically, PEAK Wind perform the following assessments:

- Review of projected AEP compared to historical realised AEP, including assessment of deviations and identification of potential optimization of production

- Comparison of expected major component failures and historical actual major component exchanges incl. expert opinion on any structural flaws

- Review of performed and planned service and maintenance of the assets incl. expert opinion on potential inadequacies

- Asset integrity assessment and subsequent estimation of remaining useful lifetime of the assets based on factors such as turbine design, site suitability, operations history, and planned maintenance regime (for further details on end-of-life strategy see PEAK Wind’s insight article “Setting an End-of-life Strategy from Day 1- Key considerations for a fact-based analysis”

When it comes to the commercial due diligence, typical requested documents include the following:

- Financial model

- Information memorandum (IM)

- Description of O&M strategy

- CAPEX and OPEX budgets including explanatory notes

- Actual financial accounts

- Key project contracts, e.g., Turbine Supply Agreement (TSA), Service Maintenance Agreement (SMA), Asset Management Agreement (AMA), Operations Management Agreement (OMA) and Balance of Plan (BoP) service incl. pricing and terms and conditions

- Insurance policies and premiums

- Historical management/performance reports

These documents are subsequently scrutinised to understand the underlying commercial/economic details behind and the contractual obligations of the assets, and conduct the following assessments:

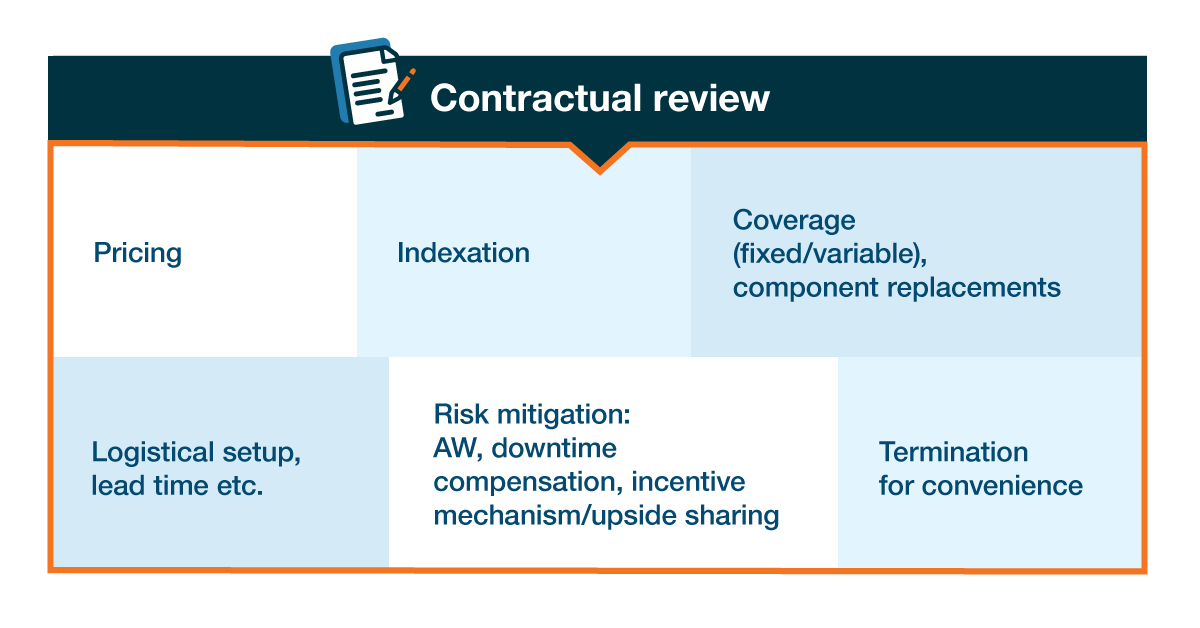

- Review of (signed) project contracts, pricing, coverage etc. incl. market benchmarking and assessment of risks and potential improvement potential

- Benchmarking of total projects costs to relevant market levels, and bottom-up modelling of OPEX budgets based on proprietary tools and algorithms

- Comparison of historical realized costs/revenue and historical projected budgets to assess the accuracy of the assumptions and subsequently review whether the financial model is appropriate.

- Review operational strategy, and provide commentary on potential inadequacies, risks or potential optimizations

- Review of key valuation assumptions such as AEP, availability, OPEX and lifetime, and provide expert commentary on the observed levels incorporating key findings from the technical due diligence

Naturally, no guarantees can be made with respect to future operations and associated OPEX levels. However, through the due diligence process and assessments, one is able to provide educated guidance on to which degree future lifetime and performance of the assets could be impacted, thus strengthening the assumptions applied in the financial model.

Common observations and trends

Through involvement in several due diligence processes in various countries and spread across multiple types of assets, it becomes apparent that certain observations are recurring across projects. The following paragraph will present an overview of a few selected common observations and outline whether any trends can be identified.

Technical observations

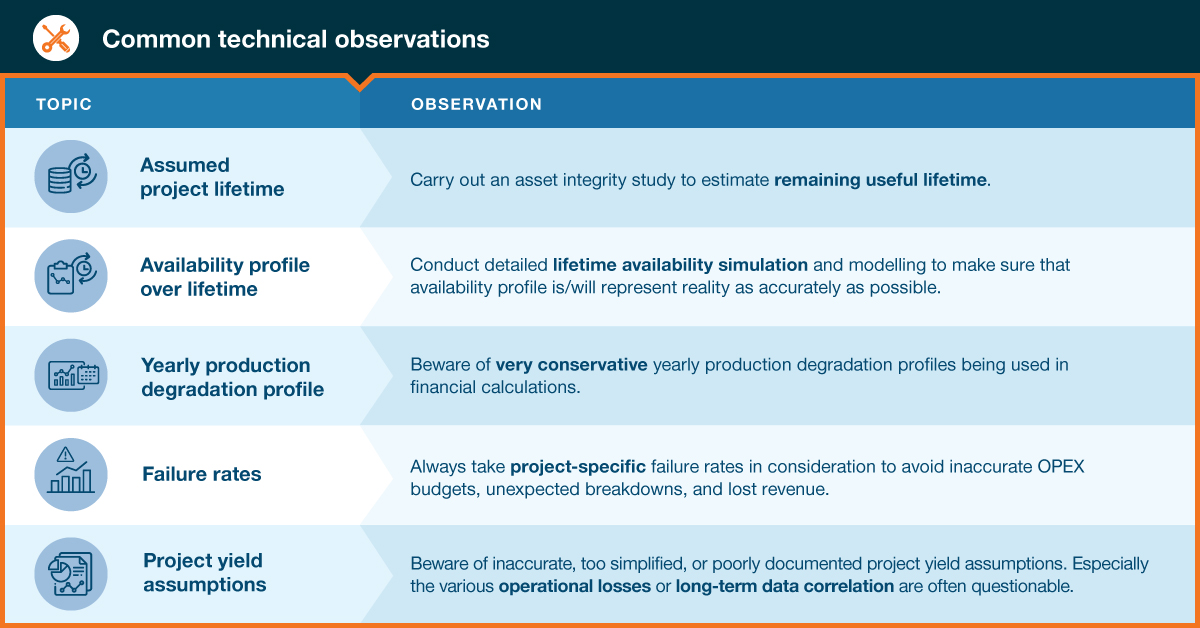

- Despite the design lifetime of wind turbines being 25 years or below, financial models often reflect a 30 or even 35-year lifetime. While this can technically be feasible, PEAK Wind always recommends an asset integrity study to estimate remaining useful lifetime. Such an assessment needs to be conducted several times and early on in projects lifetime in order to initiate preventive measures that will enable an extension of the project lifetime.

- Similarly, the availability profile over lifetime is often simplified and assumed stable at the level warranted by the service provider. PEAK Wind recommends conducting detailed lifetime availability simulation and modelling to make sure that availability profile is/will represent reality as much as possible.

- A yearly production degradation profile is often omitted from the financial model, and although it is a measurement that is notoriously difficult to quantify research indicates that degradation does occur, thus, depending on the service regime and general asset condition, it should be considered and commented on. PEAK Wind have often experienced a very conservative profile is used financial calculations.

- Failure rates, let alone project specific failure rates, are often lacking, or not considered. This can lead to inaccurate OPEX budgets and result in unexpected breakdowns, costs, and lost revenue. PEAK Wind have sufficient data points to create failure rates for most WTG platforms.

- Project yield assumptions are often inaccurate, too simplified, or poorly documented. Especially the various operational losses or long-term data correlation are questionable.

Commercial observations:

Common commercial observations include, but are not limited to the following:

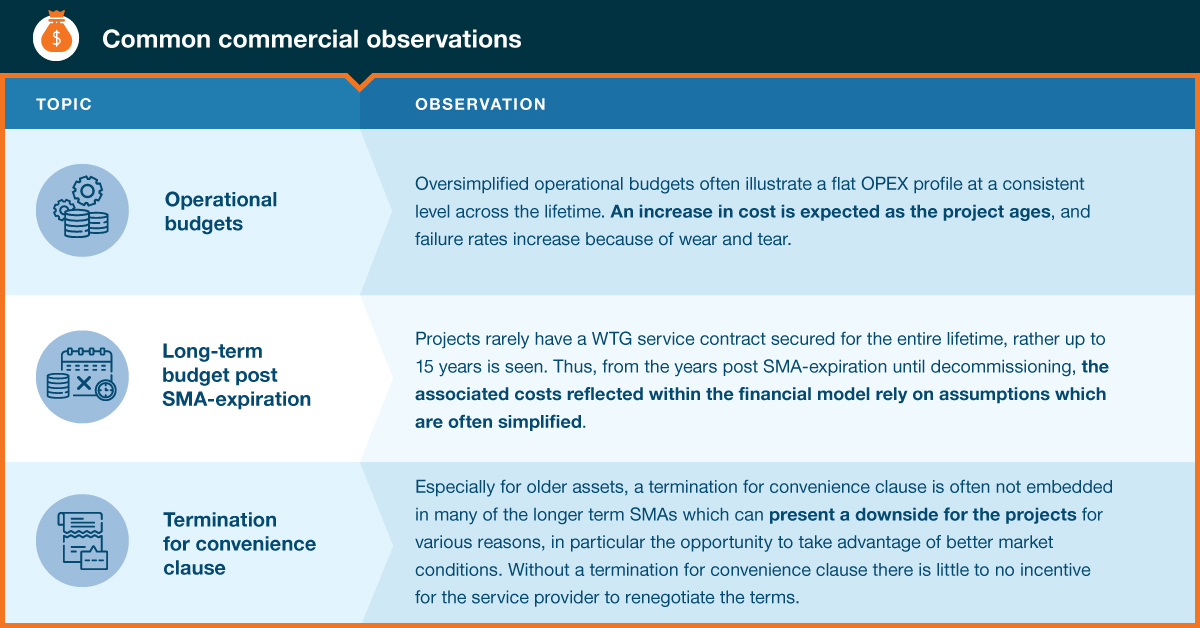

- Oversimplified operational budgets illustrating a flat OPEX profile at a consistent level across the lifetime. Unless the project is covered by a fixed price, full scope service agreement until decommissioning, an increase in cost is expected as the project ages, and failure rates increase because of wear and tear, resulting in higher frequency of component replacements.

- Projects rarely have a WTG service contract secured for the entire lifetime, rather up to 15 years is seen. Thus, from the years post SMA-expiration until decommissioning, the associated costs reflected within the financial model rely on assumptions. Similar to the point above, these assumptions are often oversimplified, and instead of relying on an analysis of price implications of extending the SMA, a flat price is often assumed. Alternatively, an assumption of a self-operating strategy (where the service activities are insourced) post SMA-expiration is often observed. Successful implementation of such a setup requires a clearly defined strategy, and an appropriate setup with a capable organization, however, the required resources and capabilities of running such a setup are often underestimated and simplified.

- Especially for older assets, a termination for convenience clause is often not embedded in many of the longer term SMAs which can present a downside for the projects for various reasons, in particular the opportunity to take advantage of better market conditions. Longer contracts typically have a duration of 15 years, wherein the prices are locked at a given level (with indexation), which depending on the age of the assets does not reflect recent price reductions caused by increased competition and general price pressure and is thus unfavourably high and skewed towards the service provider. Without a termination for convenience clause there is little to no incentive for the service provider to renegotiate the terms

Trends:

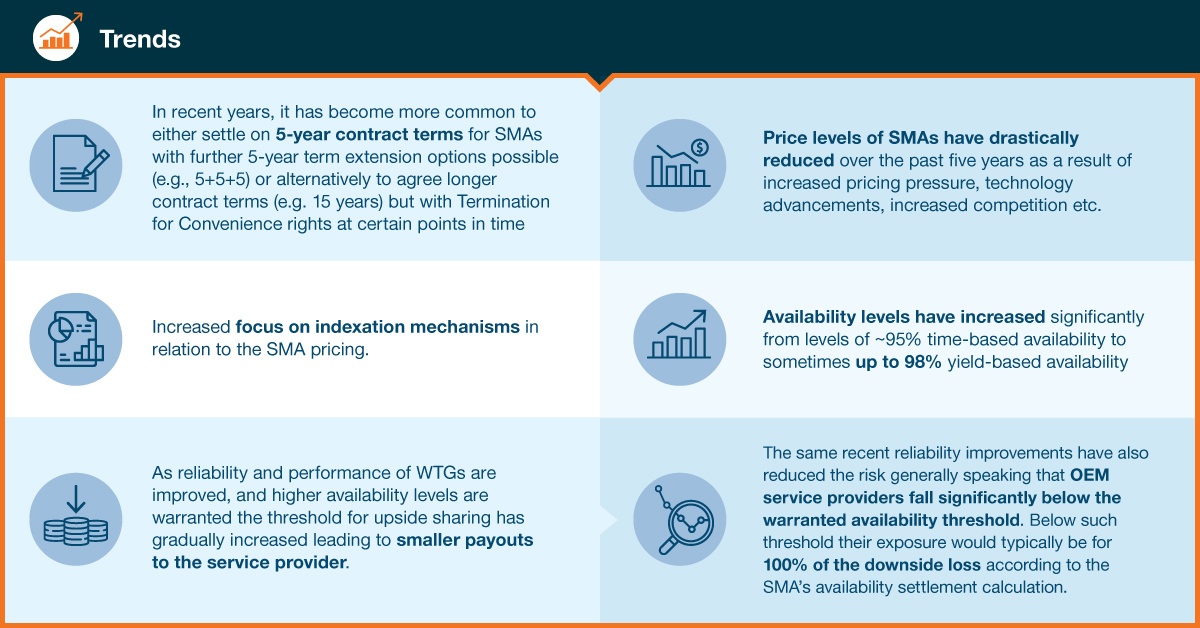

- Historically, SMAs for project financed projects have been locked in at durations of 15 to 20 years, however, in recent years it has become more common to either settle on 5 year contract terms with further 5 year term extension options possible (e.g., 5+5+5) or alternatively to agree longer contract terms (e.g. 15 years) but with Termination for Convenience rights at certain points in time (typically subject to cancellation fees based on % of remaining Annual Base Fees) and subsequently pursue an alternative setup where the service activities are either insourced or outsourced to a 3rd party provider. I.e., the dependency on the OEMs who have historically provided the servicing is reduced.

- Price levels of SMAs have drastically reduced over the past five years as a result of increased pricing pressure, technology advancements, increased competition etc. However, recent market conditions with increasing cost levels may impact this as it has become more challenging for the service providers to maintain profitability

- Focus on indexation mechanisms in relation to the SMA pricing has also increased in the same timeframe, and this trend is further strengthened by the current market developments with sky-rocketing inflation and subsequent price increases. It is essential for a project to obtain a fair indexation mechanism otherwise it is at risk of eroding the business case

- Availability levels have increased significantly from levels of ~95% time-based availability to sometimes up to 98% yield-based availability, indicating strong confidence in the reliability of the latest WTG platform technologies

- Typically, SMAs include an incentive mechanism in the form of an upside sharing, through which the service provider is entitled to a certain amount of the revenue generated as a result of reaching an availability level higher than a given threshold. As reliability and performance of WTGs are improved, and higher availability levels are warranted, the threshold for upside sharing has gradually increased leading to smaller payouts to the service provider. In addition the same recent reliability improvements have also reduced the risk generally speaking that OEM service providers fall significantly below the warranted availability threshold. Below such threshold their exposure would typically be for 100% of the downside loss according to the SMA’s availability settlement calculation.

PEAK Wind is at the forefront of the industry, and have employees specialized in all fields from engineering to contract negotiations, enabling us to provide due diligence support tailored to your project.

Keep in mind…

- Due diligence is an essential part of every successful transaction

- The due diligence process is complex and must be planned well in advance to allow for a thorough review of key documentation

- A thoroughly conducted due diligence highlights key risks and potential optimization areas and enables the investor to take a decision on an informed basis

- The due diligence itself does not solve any highlighted risks/issues nor warrant a successful transaction, rather it brings awareness and suggestions for mitigations

Want to learn more about due diligence within renewables?

Please reach out, we are always happy to answer your questions and engage in discussions on commercial and technical due diligence topics for all renewable asset classes.

Alexander Stegelmann | Head of Due Diligence & Transactional Services | Get in touch

Lene Hellstern | Director of Engineering | Get in touch

Brian Tully | Senior Manager & Country Director UK | Get in touch |